How to Get a Personal Loan (Even With Bad Credit)

Requirements, Options & Business Use Cases

A personal loan is one of the most commonly searched financing options because it offers fast access to cash without requiring collateral. But while it’s widely used, most borrowers don’t fully understand how approval works, what lenders look for, or how to use it strategically—especially for business purposes.

It's not just “quick cash.”

It’s a financial tool—and how you use it determines whether it builds your business or creates financial pressure.

This guide breaks down exactly how personal loans work, how to qualify, and how entrepreneurs are using them to fund business expenses when traditional financing isn’t available.

What Is a Personal Loan?

A personal loan is an unsecured installment loan that allows you to borrow a fixed amount of money and repay it in monthly payments over a set term, typically ranging from 12 to 60 months.

Approval is based primarily on:

Credit score and credit history

Income and employment stability

Debt-to-income ratio (DTI)

Overall credit profile and repayment behavior

Unlike business loans, personal loans do not require business revenue, collateral, or detailed business financials in most cases.

What Can a Personal Loan Be Used For?

Personal loans are flexible, which is why they are often used for both personal and business-related expenses.

Common approved uses include:

Debt consolidation

Medical expenses

Emergency costs

Home improvements

Business-related uses (when used strategically):

Many entrepreneurs use personal loans for early-stage business needs such as:

Startup costs (LLC formation, licensing, setup fees)

Website development and branding

Marketing and paid advertising

Equipment or software purchases

Initial inventory

Cash flow gaps in early business stages

While lenders issue funds personally, there are no restrictions on using the funds for business in most cases—however, repayment responsibility is tied to your personal credit.

Can You Use a Personal Loan for Business?

Yes—but it should be done strategically.

A personal loan can support business growth when:

You are in the early stages and lack business credit

You need fast access to capital

You are bridging funding gaps before qualifying for business financing

You are investing in revenue-generating activities

However, it should NOT replace long-term business financing strategies such as business credit lines, SBA loans, or revenue-based funding.

What Credit Score Do You Need for a Personal Loan?

Credit requirements vary by lender, but general ranges include:

Excellent credit (720+) → Lowest interest rates, highest approval odds

Good credit (660–719) → Competitive approval options

Fair credit (580–659) → Limited options, higher interest rates

Poor credit (below 580) → Subprime or alternative lenders only

Income stability and debt-to-income ratio can sometimes outweigh credit score alone, depending on the lender.

Can You Get a Personal Loan With Bad Credit?

Yes, but your options will be more limited and typically more expensive.

Options for bad credit borrowers include:

1. Subprime personal loans

Easier approval

Higher interest rates

Shorter repayment terms

2. Credit unions

More flexible underwriting

Relationship-based lending

3. Online alternative lenders

Fast approval decisions

Less strict credit requirements

4. Co-signed personal loans

Stronger approval odds if a co-signer has good credit

5. Credit improvement before applying

30–120 days of credit repair actions can significantly improve approval terms

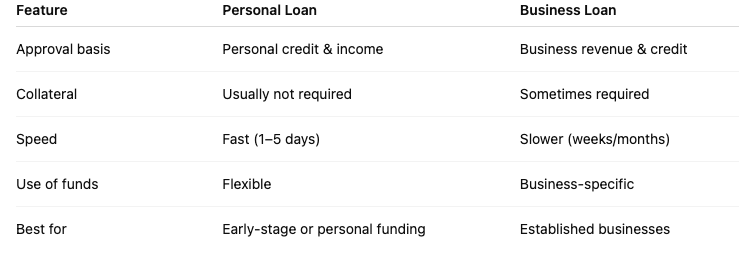

Personal Loan vs Business Loan: What’s the Difference?

What NOT to Do With a Personal Loan

Many borrowers make costly mistakes that affect long-term financial stability.

Avoid:

Using funds without a repayment plan

Mixing personal lifestyle spending with business capital

Borrowing without understanding interest costs (APR)

Ignoring monthly cash flow impact

Applying repeatedly and triggering multiple hard inquiries

Funding untested business ideas without validation

A personal loan should always be treated as structured capital, not emotional money.

What Lenders Look At Before Approving a Personal Loan

Approval is not just about credit score. Lenders evaluate:

Credit history and payment behavior

Income consistency

Employment or business stability

Debt-to-income ratio (DTI)

Recent credit inquiries

Bank account activity (in some cases)

The goal for lenders is simple:

Can you repay the loan reliably and on time?

Why People Get Denied for Personal Loans

Most denials happen for predictable reasons:

High debt-to-income ratio

Insufficient income

Poor or thin credit history

Recent late payments

Applying for the wrong lender type

Lack of documentation

Many borrowers give up after denial—but often the issue is not eligibility, it’s misalignment with the lender type.

What to Do Before You Apply for a Personal Loan

Before submitting an application, review:

Your credit profile

Your monthly income and expenses

Your repayment plan

Whether this loan supports income or growth

Whether you qualify for better funding options

Strategic borrowers don’t just apply—they position themselves first.

Next Steps

A personal loan is not just a way to access money—it’s a financial tool that can either support growth or create long-term pressure depending on how it’s used.

The difference between borrowers who struggle and entrepreneurs who scale is not access to money.

It’s strategy, timing, and structure.

Apply for Funding Support

If you're exploring funding options and want clarity on what you may qualify for, you can 👉 start here: and APPLY NOW

This helps identify funding pathways based on your current financial and business position.